Tokenization won’t make illiquid assets liquid, say executives

At Paris Blockchain Week, executives warned tokenizing real estate, private credit and other illiquid assets does not by itself create active secondary markets or trading depth.

Industry executives at Paris Blockchain Week warned that placing real-world assets on a blockchain does not automatically produce active secondary markets. The panel took place in Paris and was moderated by Yana Prikhodchenko.

Oya Celiktemur, Ondo Finance sales director for EMEA, told the audience there is a common misconception that tokenization alone makes illiquid holdings easier to trade. “I think there’s still this idea that tokenizing something illiquid will somehow magically make it a liquid asset, which is just not true,” she said, noting that assets such as real estate and private credit were limited in liquidity before tokenization.

Francesco Ranieri Fabracci, head of tokenization expansion at Tether, argued that putting assets onchain does not create trading depth. He suggested that a narrower set of instruments – bonds, money market funds and stablecoins – are more likely to see consistent liquidity when tokenized.

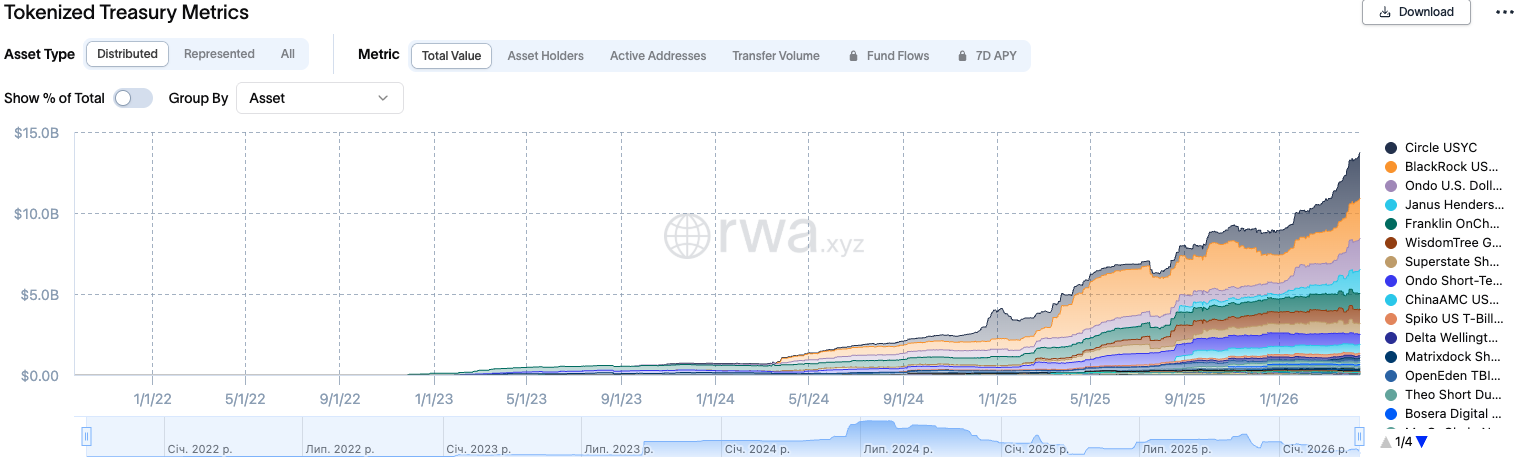

Data from analytics platform RWA.xyz show the tokenized real-world asset market (excluding stablecoins) grew from $8.8 billion on April 16, 2025, to about $29.9 billion on April 16, 2026. Growth was concentrated in standardized instruments: tokenized government bonds and commodities accounted for a large share of the market during that period. Tokenized real estate increased from roughly $35 million to $296 million, and tokenized private equity rose from about $60 million to $223 million over the same year.

Panelists and the data source cautioned that a rising outstanding market value does not prove active secondary trading. Outstanding value can climb because more tokens are issued and held, even if secondary market trading remains thin or occurs mostly through initial distribution channels.

Speakers identified practical barriers to secondary trading in traditionally illiquid assets. Real estate and private-credit investments often involve complex ownership rights, customized contractual terms and long holding periods, which can complicate fractional ownership and transfer. By contrast, standardized debt and money-market-like products typically have clearer pricing, broader investor familiarity and more frequent turnover, conditions that support trading activity.

Panelists said achieving regular secondary-market trading will require coordinated changes in trading venues, market making, legal frameworks, custody and transfer processes, and a broader base of buy-side participants willing to trade. They also called for transparent data and market infrastructure that measure secondary activity separately from issuance figures.

The discussion noted that tokenization can enable fractional ownership and programmable settlement, but panelists emphasized that token formats alone do not guarantee liquidity.

The material on GNcrypto is intended solely for informational use and must not be regarded as financial advice. We make every effort to keep the content accurate and current, but we cannot warrant its precision, completeness, or reliability. GNcrypto does not take responsibility for any mistakes, omissions, or financial losses resulting from reliance on this information. Any actions you take based on this content are done at your own risk. Always conduct independent research and seek guidance from a qualified specialist. For further details, please review our Terms, Privacy Policy and Disclaimers.

Articles by this author