Online platforms and the shift toward instant payments

Five years ago, waiting 3–5 business days for a withdrawal was widely accepted. Today, users expect funds in minutes, and platforms that can’t deliver lose customers to those that can.

Instant payments shifted from a premium feature to table stakes across e-commerce, trading platforms, subscription services, and regulated online gaming. The challenge now is choosing the right rails and managing the costs.

The rising demand for real-time payments in digital services

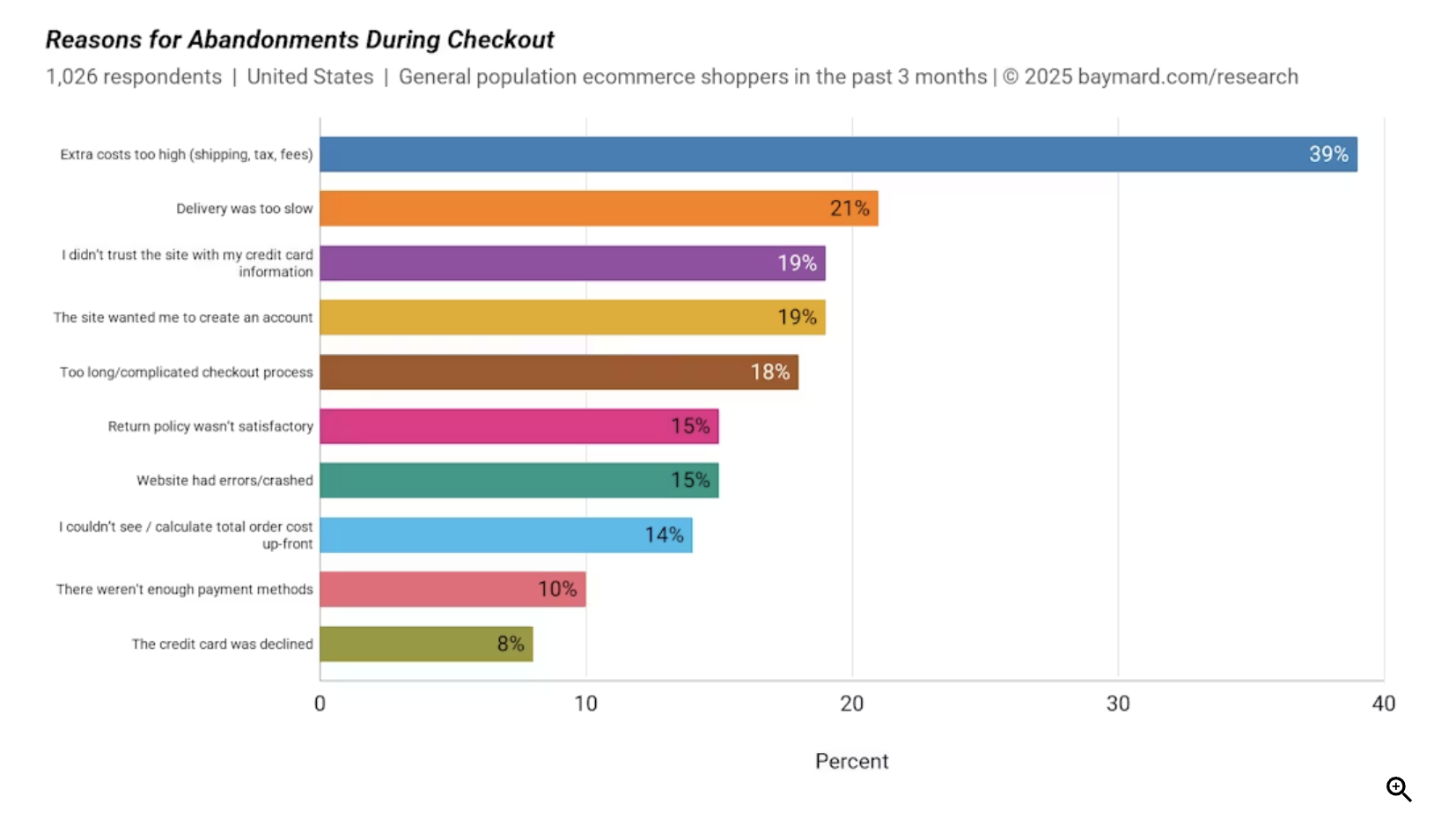

User expectations moved faster than payment infrastructure. According to Baymard Institute research, 10% of online shoppers abandon checkout if their preferred payment method isn’t available. Withdrawal speed ranks second only to fees in satisfaction surveys for transaction-heavy platforms.

Instant payment methods became competitive differentiators in sectors where users move money frequently. Trading platforms that settle crypto withdrawals in under 10 minutes gain market share over competitors still processing in 24-48 hours. Gig economy apps that pay workers same-day see higher driver retention than those paying weekly. Subscription platforms offering instant refunds reduce support ticket volume by 40% compared to 7-10 day processing windows.

This shift is supported by infrastructure such as FedNow in the U.S. (launched mid-2023), the UK’s Faster Payments Service expansion, and Brazil’s PIX system processing 34 billion transactions in 2024, up 75% year-over-year. Platforms either integrate or watch users leave for those that did.

The technical challenge is that instant settlement requires real-time liquidity management, fraud detection systems that make decisions in milliseconds, and a settlement infrastructure that doesn’t break down when the bank’s API goes down at 2 a.m. on a Saturday. Platforms that figured this out early absorbed higher processing costs to build user bases. Competitors trying to catch up now face steeper switching costs.

Cross-border payments and crypto integration

Traditional correspondent banking still moves most international money, and it still takes days. A SWIFT transfer from Germany to Thailand touches 3-4 intermediary banks, takes 2-5 days, and costs $25-50 in fees that nobody explains in plain language. Instant payments broke that model two ways: blockchain rails and stablecoin settlement.

USDC and USDT settle cross-border transfers in under 5 minutes at costs below $1 for amounts up to six figures. Platforms serving international freelancers, remote teams, and cross-border e-commerce adopt stablecoins for speed and cost, not ideology. A designer in Argentina receiving payment from a U.S. client used to wait a week and lose 5-8% to fees and FX spreads. With USDC on Polygon, settlement happens in 90 seconds and costs $0.02.

Crypto integration addressed a problem traditional rails struggled with: 24/7 availability. Banks close. Blockchain networks run continuously. Platforms operating across time zones can’t tell users in Tokyo that their Friday night withdrawal won’t process until Monday morning in New York. Stablecoin rails run all weekend. Platforms that implemented them report 30-40% higher weekend transaction volume compared to bank-dependent competitors.

Regulatory clarity improved enough that mainstream platforms integrate crypto without reputational risk. Coinbase Commerce, BitPay, and MoonPay provide plug-and-play infrastructure. A mid-sized e-commerce platform can add stablecoin checkout in under two weeks of dev work. The friction is deciding whether your user base wants it and your compliance team can manage it.

High-volume digital industries adopting instant models

E-commerce platforms moved early. Amazon processes refunds to original payment methods in under 24 hours for most transactions. Shopify merchants offering instant refunds see 22% fewer payment disputes compared to those using standard 5-7 day windows, according to internal data shared at their 2024 developer conference.

Trading platforms depend entirely on instant settlement. A user who sells a position and can’t withdraw funds for 48 hours will move to a platform where withdrawal takes 8 minutes. Robinhood’s instant deposit feature (funds available immediately, settlement happens in background) became their primary growth driver in 2020-2021. Competitors that didn’t match it lost users.

Subscription services face a different challenge. Recurring billing requires instant payment confirmation to avoid service interruptions. Netflix, Spotify, and subscription box services moved to real-time payment verification. If your card declines, they know within seconds and can retry or notify you before your service lapses.

Regulated online gaming platforms, specifically licensed operators in jurisdictions like the UK, Malta, and New Jersey, adopted online payment methods that prioritize speed and transparency. Players deposit, play, and withdraw in sessions that often span hours. Platforms like Bet365 process most withdrawals to e-wallets in under 24 hours and debit cards in 1-5 days, with exact timing disclosed upfront. Competitors still processing in 5-7 days lose users. Regulatory requirements around responsible gambling also push instant payments: a user who requests withdrawal should see funds leave the platform quickly, reducing the temptation to reverse and continue playing.

High-frequency transaction environments show the same pattern: payment speed directly impacts user retention and platform economics.

Payment transparency and platform comparisons

Users don’t trust vague timelines. “Withdrawals processed within 3-5 business days” means nothing when competitors specify “usually under 4 hours, maximum 24.” Transparency became a competitive requirement.

Independent comparison platforms emerged to help users evaluate payment speed, supported methods, and fee structures across digital services. These resources aggregate data from user reviews, public disclosures, and direct testing to rank platforms on payment reliability. A platform that claims instant withdrawals but consistently delivers in 18-24 hours gets flagged quickly.

Marketing can claim speed, but user reviews and independent testing expose gaps between claims and reality. Fintech platforms, e-commerce marketplaces, and online entertainment services face the same scrutiny: if you advertise instant payments, users will test it, document it, and share results.

The shift forced platforms to improve internal operations. Real-time payment status dashboards, automated KYC to reduce manual review delays, and better communication around processing times became standard. Users compare platforms on whether withdrawals actually happen when promised, not just on features and fees.

Instant payments became infrastructure, not a feature. Platforms that haven’t upgraded yet explain why they’re still slow while users switch to competitors offering settlement in minutes. By 2026, “we’re working on it” won’t retain customers.

The material on GNcrypto is intended solely for informational use and must not be regarded as financial advice. We make every effort to keep the content accurate and current, but we cannot warrant its precision, completeness, or reliability. GNcrypto does not take responsibility for any mistakes, omissions, or financial losses resulting from reliance on this information. Any actions you take based on this content are done at your own risk. Always conduct independent research and seek guidance from a qualified specialist. For further details, please review our Terms, Privacy Policy and Disclaimers.

Articles by this author