Best crypto cards in 2026 – a test of fees, cashback, and usability

A flashy metal card and a promise of “5% cashback” look great on a landing page. But when you are standing at a checkout counter abroad, the only things that matter are: Will the transaction go through? And how much will the hidden fees actually cost you?

We don’t trust marketing brochures. We trust receipts.

For this ranking, our team applied for the most popular crypto debit cards on the market, completed the KYC, and waited for the physical delivery. Once activated, we loaded each card with $200 of our own capital. And didn’t just let the funds sit there – we used them.

Over a two-week period, we treated these cards as our daily drivers. We bought coffee to test transaction speeds, made online purchases to check 3D Secure reliability, spent money in foreign currencies to catch hidden FX spreads, and withdrew cash from ATMs to see if the “free withdrawal” limits were real.

Here is what we found when we stopped reading the fine print and started swiping.

Understanding сrypto сards and their use

A crypto card is essentially a bridge that connects your digital wallet to the traditional financial world. While it looks and functions exactly like a standard Visa or Mastercard issued by your bank, the underlying engine is different. Instead of drawing funds from a checking account, it draws from your cryptocurrency balance.

This means you can buy groceries with Bitcoin or pay for dinner with USDT, even if the merchant has no idea what “crypto” is. The card handles the complexity in the background, allowing you to spend digital assets at any of the 100+ million locations worldwide that accept payment cards.

How the conversion works

When you tap your card to buy a $5 coffee, the merchant wants $5, not 0.00005 BTC. The conversion happens in one of two ways, depending on the card:

- Pre-paid (top-up) model. You manually sell your crypto for fiat currency (USD, EUR, GBP) within the card’s app before you shop. You are essentially loading a prepaid debit card. This gives you control over the exact exchange rate.

- Real-time conversion. You hold crypto in your wallet until the exact moment of purchase. When you swipe the card, the issuer instantly sells the exact amount of crypto required to cover the fiat cost.

Note: While convenient, real-time conversion often incurs a “spread” or conversion fee, which we carefully measure in our testing.

The basic usage flow

Finding the best crypto cards isn’t just about the plastic; it’s about the workflow. Here is the typical lifecycle of using one:

- Top-up: You transfer crypto (e.g., USDT, BTC) from your private wallet or exchange account to the card’s funding wallet.

- Spend: You use the card physically or virtually. The network (Visa/Mastercard) authorizes the transaction in fiat.

- Settlement: The card issuer deducts the equivalent crypto from your balance.

A few seconds later, you typically receive cashback (ranging from 1% to 8%) deposited directly back into your crypto wallet.

Types of crypto cards available today

When searching for the best crypto debit card, you quickly realize that not all plastic is created equal. The market has splintered into different categories, each serving a specific type of user. Before you apply, it is critical to understand the architecture behind the card, as it dictates who actually holds your money.

1. Debit vs. credit models

Most cards on the market are actually prepaid debit cards. You are spending your own money.

- Crypto debit (prepaid): You load the card with crypto (or convert it to fiat balance) and spend it. If you have $500 in your account, you can spend $500. This is the model used by Binance, Bybit, and Crypto.com. It is simple, effectively “cashing out” your crypto transaction by transaction.

- Crypto credit: These are rarer. Instead of selling your crypto, the issuer freezes it as collateral and lends you fiat to spend. You pay the credit card bill later. The advantage? You don’t trigger a taxable event (selling crypto) every time you buy lunch. The risk? If the market crashes, your collateral might get liquidated to pay the debt.

2. Custodial vs. non-custodial

This is the single biggest security distinction.

- Custodial cards (the standard): You deposit your funds into the issuer’s wallet (e.g., your Binance funding wallet). The exchange holds the private keys.

- Pros: Instant conversion, easy recovery if you lose your password, high transaction speeds.

- Cons: “Not your keys, not your coins.” If the exchange freezes, your card stops working.

- Non-custodial (DeFi) cards: You connect your own self-custody wallet (like MetaMask or Ledger) to the card. The issuer never holds your funds until the exact moment of the transaction.

- Pros: You maintain absolute control over your assets.

- Cons: Often requires complex smart contract approvals and higher gas fees for top-ups.

3. Virtual vs. physical cards

In our testing, we found distinct use cases for both form factors.

- Virtual cards: Issued instantly upon approval. These live in your app and can usually be added to Google Pay or Apple Pay immediately. They are safer for online shopping – if compromised, you can terminate them instantly and generate a new one for free.

- Physical cards: The plastic (or metal) card that arrives in the mail. You need this for one specific reason: ATM withdrawals. While contactless payment is common, cash is still king in many places, and you cannot withdraw cash with a virtual card.

Which one is the “Best Crypto Card” for you? For 90% of users, a custodial debit card offers the smoothest experience – it feels exactly like using a bank card, but funded by your crypto gains. Non-custodial options are powerful, but generally reserved for advanced DeFi natives who refuse to trust centralized exchanges.

Top crypto cards by use case

We looked for the right tool for the job. A card that is perfect for a DeFi native might be a nightmare for someone who just wants to spend their USDT earnings on groceries.

To find the best cryptocurrency card, we subjected every contender to the same $200 stress test. We loaded them with funds, checked the speed of the “crypto-to-fiat” bridge, and calculated the actual value of the rewards after fees. We specifically looked for cards that excel in critical categories: maximum cashback rewards, seamless daily spending, EU-specific compliance, non-custodial security, and multi-chain flexibility.

Here are the five cards that survived our wallet test, ranked by how they perform in the real world.

WhiteBIT Nova Card

Score: 4.5/5

We tested the Nova Card as a daily driver for a user living within the Eurozone. Unlike some competitors that require you to pre-sell crypto into a fiat wallet, this card spends directly from your WhiteBIT exchange balance, converting crypto to Euros at the moment of purchase. The spice of this convenience is the conversion spread. While WhiteBIT advertises “no fee” for payments, we noted an internal exchange rate spread of up to 1% during checkout. This is the invisible cost of instant liquidity. However, the virtual card is issued instantly and works flawlessly with Apple Pay and Google Pay, allowing you to buy coffee minutes after passing KYC.

Benefits

- Instant utility: We went from approved KYC to buying groceries with Apple Pay in minutes. No waiting for plastic mail.

- Strategic cashback: You can select three categories to earn on, including a massive 10% on subscriptions (Netflix, Spotify) and 5% on Taxis.

- Zero monthly fees: Unlike traditional bank cards that nickel-and-dime you, opening and maintaining the Nova card costs €0.

Limitations

- The €25 ceiling: The cashback percentages look huge, but the monthly cap is low. If you spend heavily, you maximize your rewards very quickly.

- Geo-fenced: It is strictly for residents of 31 European countries (EEA) and Ukraine. If you are in the US or UK, this card is off-limits.

- Physical card cost: While the virtual card is free, ordering the plastic version hurts. Standard delivery costs €12–€20 (taking up to 10 days), and DHL Express can run up to €40.

Best for

European freelancers and digital nomads who earn in crypto and want to spend their income instantly on rent, subscriptions, and daily life without managing a separate bank account.

Strengths:

- High spending limits: With a daily spending cap of €10,000 and a monthly limit of €25,000, this card can actually handle real-life expenses, not just small purchases.

- Category flexibility: We loved the ability to change cashback categories daily. You can switch to “Travel” before booking a flight and “Food” for the weekend.

- Asset support: It spends directly from 12 core assets, including BTC, ETH, SOL, USDC, EURI, covering the vast majority of user portfolios.

Weaknesses:

- ATM friction: Cash is expensive. Withdrawals cost a fixed €3 inside the EEA, and €3 + 2.2% internationally.

- Regional mismatches: We encountered friction with services like Spotify, where payments were declined because the card’s issuing country didn’t match the Spotify account region.

- Support speed: While generally helpful, complex questions about AML freezes can take time to resolve, leaving funds temporarily inaccessible.

Fold Card

Score: 3.9/5

The Fold Card is less of a traditional debit card and more of a Bitcoin rewards game attached to a checking account. We tested it as our primary spending vehicle for a week, funding it via ACH and routing everyday purchases through it. The premise is simple: you spend dollars, you earn Satoshis. The “nerdy” reality, however, is the variance. Unlike a flat 2% card, Fold uses a “Spinwheel” mechanic after each purchase. In our test, this meant some coffees earned massive rewards while others earned almost nothing. It adds a layer of volatility to your cashback. Furthermore, the “Bill Pay” feature – the card’s killer app – relies on the ACH network, meaning payments aren’t instant and can take 1–4 business days to settle.

Benefits

- Rewards that appreciate: Unlike cash that loses value to inflation, earning rewards in Bitcoin means your cashback potential grows (or shrinks) with the market.

- The “Bill Pay” loophole: For Fold+ subscribers, this is the only easy way we found to earn rewards on major flat-rate expenses like rent, mortgage, and tax bills.

- Gift card arbitrage: If you are willing to buy gift cards in the app before you shop (e.g., for Amazon or Uber), the reward rates can jump significantly higher than standard swipes.

Limitations

- The subscription wall: To unlock meaningful rewards and Bill Pay, you essentially must pay for Fold+ ($10/mo or $100/yr). The free tier feels severely handicapped.

- US-only hard stop: This is strictly for US residents with an SSN. No global access.

- Withdrawal friction: When we tried to move our earned Bitcoin to a cold wallet, we hit a security hold. Expect a 3–7 day delay before your coins are truly yours.

Best for

US-based Bitcoin maximizers who want to squeeze rewards out of their largest monthly bills (rent/mortgage) and enjoy the “lottery” aspect of gamified spending.

Strengths:

- Rent rewards: We successfully tested the Bill Pay feature on a large payment. While slow (ACH), getting Bitcoin back on a mortgage payment is a unique utility in the market.

- Zero-fee buying: Fold+ users get a “zero-fee” Bitcoin buying option in the app, which is a nice perk for DCA (Dollar Cost Averaging) strategies.

- Insurance structure: Fiat funds are FDIC-insured through a partner bank, and Bitcoin custody is backed by BitGo insurance, providing a safety net for held assets.

Weaknesses:

- “Luck” Factor: The Spinwheel is fun until you hit a low spin on a big purchase. The lack of a guaranteed high fixed rate can be frustrating for those who want predictability.

- Slow Rails: Funding the card and paying bills runs on legacy banking rails. Waiting 4 days for a transfer to clear feels archaic compared to crypto-native speeds.

- Support Black Hole: We found support to be email-only and slow. If your account gets flagged or a transaction stalls, don’t expect a quick live chat resolution.

Coinbase Card

Score: 3.7/5

The Coinbase Card is the ultimate convenience play for users already in the ecosystem. We tested both the virtual and physical cards, linking them to USD and crypto balances. The standout feature is the “Paying with” toggle, which lets you switch funding sources (e.g., from USDC to Bitcoin) in one tap. Tax structure demands a closer look. In the US, every time you buy a coffee with Bitcoin using this card, you are triggering a taxable event (selling property). Coinbase handles the conversion instantly, but the transaction history shows two distinct steps: a crypto sale (with a spread) and a fiat payment. If you spend USD (USDC), it behaves like a standard debit card; if you spend BTC, you are effectively paying a conversion fee + capital gains tax on every swipe.

Benefits

- Rotational rewards: You don’t just earn points; you earn crypto. We selected our reward asset from a rotating list (BTC, ETH, USDC), effectively allowing us to Dollar Cost Average (DCA) with every purchase.

- No annual fees: Unlike premium travel cards, there is no issuance fee, no monthly maintenance fee, and no foreign transaction fee charged by Coinbase itself.

- Instant freeze: The security controls are robust. We tested the “Lock Card” feature, and it instantly declined subsequent transactions, providing peace of mind against theft.

Limitations

- The “hidden” spread: While they claim “no transaction fees,” paying with crypto incurs a spread markup. You are selling your coins at a slightly worse rate than the market price.

- Strict daily limits: The spending limit is capped at $2,500 per 24 hours. This is fine for groceries but useless for booking a family vacation or buying high-end electronics.

- Data security history: While the card itself is safe (issued by Pathward, FDIC-insured), Coinbase’s history of support-based social engineering attacks (like the 2025 incident) is a reminder to keep your main savings in cold storage, not on your card balance.

Best for

US-based Coinbase users who want to spend their USDC balances (to avoid tax/spread drag) while earning rewards in volatile assets like Bitcoin or Ethereum.

Strengths:

- Mobile wallet parity: Adding the card to Apple Pay was flawless. We didn’t need the physical card to start spending in stores immediately after approval.

- USDC utility: When funding with USDC, the card effectively becomes a fee-free debit card that still earns crypto rewards, bypassing the conversion spread entirely.

- App UX: The interface is polished. Tracking rewards, changing funding sources, and reviewing transaction history is intuitive and fast.

Weaknesses:

- Low ATM limits: You can only withdraw $1,000 cash per day. If you are traveling and need significant cash, this card will bottleneck you.

- Variable reward rates: The reward offers change. One month you might get 4% in XLM, the next month it might drop to 1%. You have to constantly check the app to ensure you are getting value.

- Geo-restrictions: It is unavailable in a long list of sanctioned or restricted countries (China, Turkey, Venezuela), making it less reliable for global nomads than some competitors.

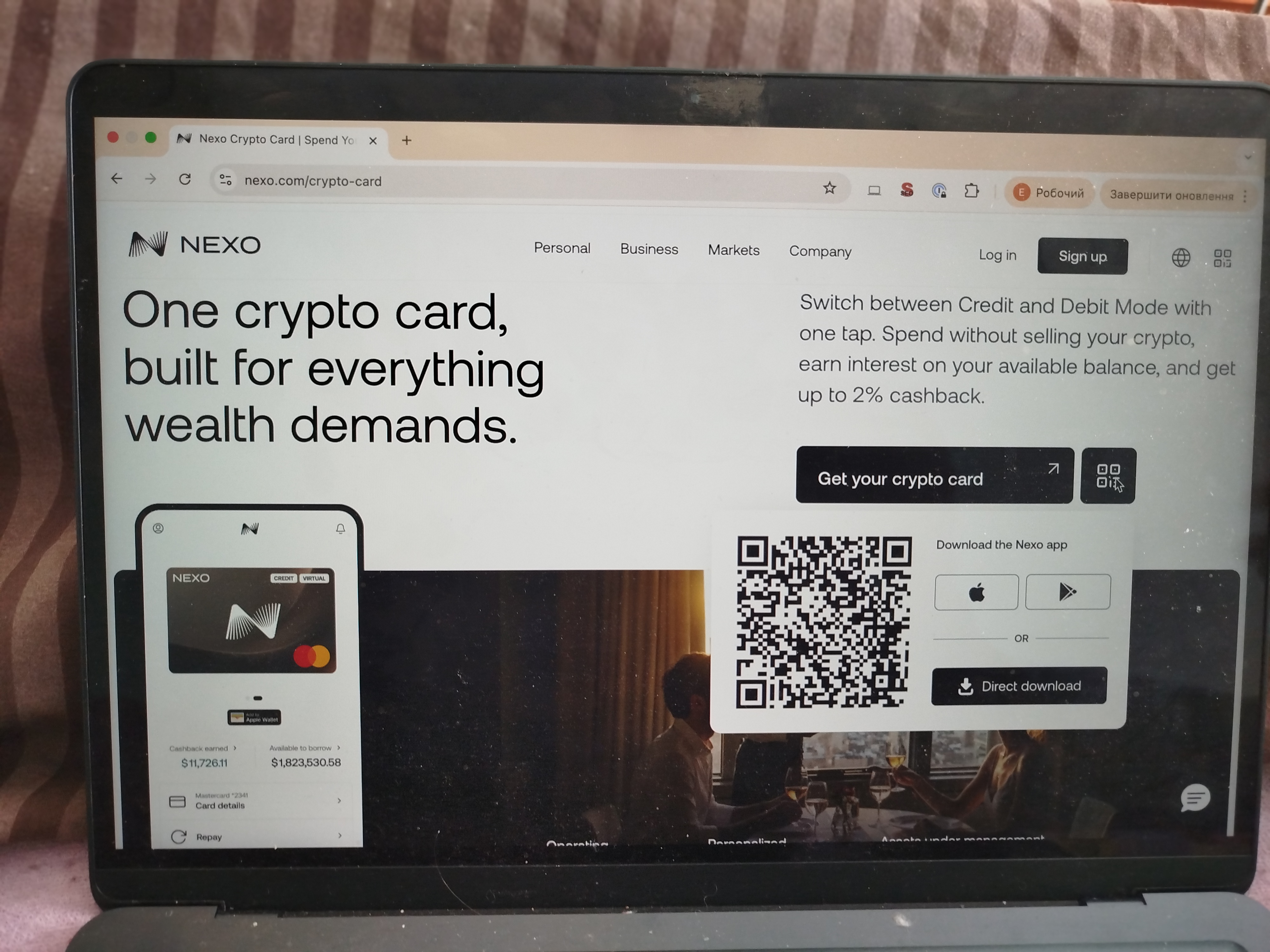

Nexo Card

Score: 3.7/5

The Nexo Card is a toggle switch between spending your cash and borrowing against your crypto. We tested the card’s dual personality by switching between modes for different transaction types. In Debit Mode, it functioned like a standard prepaid card. In Credit Mode, we executed purchases that instantly opened a loan against our portfolio. What stands out here is the Loan-to-Value (LTV) mechanics. When you buy a coffee in Credit Mode, you aren’t spending $5; you are locking up ~$20 of Bitcoin as collateral to borrow $5. If the market crashes on a Monday after a weekend of spending, your LTV spikes, potentially triggering a repayment or liquidation. It turns your credit card bill into a margin position.

Benefits

- The toggle: It is the only card on this list that lets you choose per-transaction: “Spend my stablecoins” (Debit) or “Borrow against my Bitcoin” (Credit).

- Virtual first: We verified that you can spin up a virtual card and add it to Apple Pay/Google Pay immediately, removing the wait for physical mail.

- Low barrier to entry: There are no monthly or inactivity fees for the standard tier, making it easy to keep as a secondary travel or backup card.

Limitations

- Weekend FX surcharge: If you travel, be warned: foreign exchange fees are higher on weekends. Your Saturday dinner abroad effectively costs more than your Tuesday lunch.

- Geo-fenced: Like many competitors, it is strictly limited to residents of the EEA and the UK.

- Tiered rewards: The headline cashback rates (up to 2%) are only available if you are in the “Platinum” loyalty tier (holding significant NEXO tokens). Base users earn much less.

Best for

European crypto natives who want the option to borrow for purchases during a bull market (to avoid selling appreciating assets) but switch to safe debit spending during downturns.

Strengths:

- Liquidity without tax events: In Credit Mode, you technically aren’t selling crypto, which can have tax advantages in certain jurisdictions (though you must verify with a tax pro).

- ATM scalability: The free withdrawal limits scale up nicely with your loyalty tier, making it a viable cash source for frequent travelers who hold NEXO.

- Seamless integration: The app allows you to manage the credit line health instantly, giving you a clear view of your LTV before you swipe.

Weaknesses:

- Liquidation risk: Beginners often underestimate Credit Mode. Using it for groceries implies you are comfortable managing a collateralized debt position.

- Regulatory baggage: While the card works fine, Nexo’s history of regulatory settlements (SEC in 2023, Bulgaria raids/claims) suggests a higher platform risk than a standard bank.

- Complex fee structure: Between FX fees, borrowing interest (if not Platinum), and LTV ratios, figuring out the true cost of a purchase in Credit Mode requires a spreadsheet.

Bybit Card

Score: 3.6/5

The Bybit Card is a practical “spending float” for users who already live inside the Bybit ecosystem. We approached the Bybit Card not as a bank replacement, but as a bridge for exchange funds. The setup is virtual-first: we issued a card instantly and started spending. Auto-Conversion mechanics shines here. If you spend 50 EUR while holding Bitcoin, the card engine sells exactly 50 EUR worth of BTC at that moment. While convenient, this triggers a “conversion spread” plus potentially a crypto conversion fee (depending on your region). In our tests, spending directly from a fiat or stablecoin balance was significantly cheaper than spending volatile crypto, where the invisible costs of conversion ate into the rewards.

Benefits

- Stablecoin efficiency: If you fund the card with USDT or USDC, the transaction logic is clean. You avoid the volatility risk and conversion spreads that plague Bitcoin-funded purchases.

- Virtual-first onboarding: There is no need to wait for plastic. We spun up a virtual card for online use immediately, making it a great low-commitment tool for testing the waters.

- Exchange native: It removes the friction of “withdrawing to bank.” Your trading profits become spending power instantly, without the 1-3 day ACH/SEPA delay.

Limitations

- Regional Fragmentation: There is no single “Bybit Card.” The fees, limits, and ATM rules vary wildly by country. What is free in one region might cost 2% in another.

- Regulatory Volatility: Bybit has a history of exiting or being restricted in major markets (France, UK, Malaysia). Holding large balances here carries a jurisdiction risk that self-custody cards do not.

- Fee Stacking: If you aren’t careful, you can get hit with a triple whammy: a crypto conversion fee + a foreign exchange (FX) fee + an ATM fee all on a single transaction.

Best for

Active Bybit traders who want to off-ramp their USDT/USDC profits into daily spending without leaving the exchange ecosystem.

Strengths:

- The “Spend Bucket” model: It works perfectly as a segmented spending account. We kept $200 in USDT separate from our trading margin, treating it effectively as a prepaid travel card.

- Reward promos: While complex, the rewards system often features “boosts” for specific categories. If your spending habits align with the current promo, the cashback can be competitive.

- App integration: Managing the card inside the main trading app is seamless. You can freeze the card or check your PIN in the same interface where you check your BTC positions.

Weaknesses:

- Jurisdiction risk: The card’s availability is at the mercy of local regulators. History (UK, France, Netherlands) shows that access can be cut off quickly.

- ATM “gotchas”: The free ATM allowance is usually small. Once crossed, the percentage-based fees make cash withdrawals surprisingly expensive.

- Conversion spreads: Spending volatile assets (BTC/ETH) is not efficient. You are effectively market-selling your coins at a spread for every sandwich you buy.

Final verdict: best crypto card for you

If you’re a European freelancer or digital nomad

Choose: WhiteBIT Nova Card

It’s the closest thing to a “crypto bank account” for the EEA and Ukraine. The instant virtual card lets you spend earnings immediately, and the high limits (€10k/day) mean you can actually live on it as on the best crypto card. Just watch out for the low €25 monthly cashback cap.

If you want to stack Bitcoin on rent and mortgage

Choose: Fold Card

For US residents, this is the only card that turns your biggest boring bills into Bitcoin rewards via the Bill Pay feature. The “Spinwheel” adds a fun (if volatile) gamification layer to everyday coffee runs, but the real alpha is earning on your mortgage.

If you already live inside the Coinbase ecosystem

Choose: Coinbase Card

The integration here is flawless. You don’t need to preload a card; you just toggle “Pay with USDC” and tap your phone. It’s perfect for users who want a low-friction off-ramp and the flexibility to rotate their reward currency between BTC, ETH, and others.

If you want to spend without selling your stack

Choose: Nexo Card

The “Credit Mode” toggle is a game-changer for HODLers. It allows you to borrow against your Bitcoin at the point of sale rather than selling it, avoiding taxable events. It’s a powerful tool for sophisticated users in Europe who understand loan-to-value ratios.

If you mainly spend stablecoin profits

Choose: Bybit Card

If you view your card as a way to spend trading gains, Bybit is the most efficient pipe. Funding with USDT or USDC avoids the messy conversion spreads of spending volatile assets, making it a reliable “spending float” for active traders.

Best crypto cards 2026 – side-by-side comparison

| Card | Standout | Fees | Assets | Regions | Rewards | Best for |

|---|---|---|---|---|---|---|

| WhiteBIT Nova | Instant virtual card with Apple/Google Pay | Free virtual issuance; ~1% conversion spread; €2+ ATM fee | 11 Core Assets (BTC, ETH, USDC, EURI) | 31 EEA Countries + Ukraine | Up to 10% on subs, 5% taxi (Capped at €25/mo) | European freelancers who want high limits and instant usability |

| Fold Card | “Bill Pay” rewards for mortgage & rent | Free tier or $100/yr (Fold+); foreign transaction fees apply | USD funding (Rewards paid in BTC) | US Residents Only | Variable “Spinwheel” or fixed rates; Bill Pay earning | US Bitcoin maximizers who want to gamify their spending |

| Coinbase Card | Seamless funding from exchange balance | $0 issuance; spread applies on crypto spend (none on USDC) | Spend any asset on Coinbase | US focus (Restricted in sanctioned nations) | Rotating crypto rewards (typically 1–4%) | Coinbase users wanting a low-friction USDC spending tool |

| Nexo Card | “Dual Mode” toggle (Credit vs. Debit) | No monthly fee; FX fees (higher on weekends); interest on credit | Collateralized spend (Credit) or Stablecoins/Fiat (Debit) | EEA and UK | Up to 2% in NEXO or BTC (Tier-dependent) | HODLers who want to borrow against assets rather than sell |

| Bybit Card | Efficient off-ramp for trading profits | Varies by region; Crypto conversion + FX + ATM fees often stack | Spends directly from Bybit balance | Varies by card program & region | Tiered cashback & category boosters | Active traders spending stablecoin profits directly |

Methodology – why you should trust us

We use a weighted, category-based model, collect standardized data from each card issuer (public terms + hands-on testing), and convert that into a 1.0–5.0 star score in 0.1 increments.

Our focus is practical usability: real fees, actual cashback value, regional availability, and whether the card works when you need it most.

How we collect data

- Public data: issuance fees, FX rates, ATM limit tables, supported assets, and restricted country lists.

- First-hand testing: we order the card, complete KYC, load it with $200 (crypto or fiat), make 10–15 purchases (online and in-store), test foreign currency transactions to catch hidden spreads, and verify withdrawal limits at physical ATMs.

We do not audit issuer solvency or guarantee regulatory compliance in all jurisdictions. These scores reflect practical usability and cost efficiency today.

Categories & weights

- Fees & Costs – 25%

- Rewards & Cashback – 20%

- Supported Currencies & Regions – 15%

- Card Limits & Spending Controls – 15%

- Security & Fraud Protection – 10%

- User Experience & App Integration – 10%

- Customer Support & Card Delivery – 5%

The material on GNcrypto is intended solely for informational use and must not be regarded as financial advice. We make every effort to keep the content accurate and current, but we cannot warrant its precision, completeness, or reliability. GNcrypto does not take responsibility for any mistakes, omissions, or financial losses resulting from reliance on this information. Any actions you take based on this content are done at your own risk. Always conduct independent research and seek guidance from a qualified specialist. For further details, please review our Terms, Privacy Policy and Disclaimers.

Articles by this author