Liquidations: what is ADL and why even CEXs use it

On October 11, 2025, the crypto market experienced the largest single-day liquidation volume in its history – around $19 billion was liquidated in just a few hours. Hyperliquid traders had it the worst: according to CoinGlass data, the platform liquidated $10.3 billion – more than Binance ($2.4 billion) and Bybit ($4.6 billion) combined.

Another noteworthy point is that many users of Hyperliquid DEX discovered that the exchange forcibly closed their profitable positions. And this was done through the Auto-Deleveraging (ADL) mechanism. About 35,000 positions belonging to 20,000 traders were affected.

ADL is the automatic closing of profitable traders' positions when their losing counterparts' account balances become negative. This way, the platform guarantees it won't accumulate bad debt. If you’re in profit, be aware that your funds may be used to maintain the platform’s overall security. The only ones who don't participate in auto-deleveraging are traders with no open positions.

On October 11, 2025, Hyperliquid activated the ADL mechanism for the first time in two years, liquidating profitable positions of 20,000 users. This is not a bug; it is a built-in protection mechanism designed to prevent exchange insolvency.

How ADL works and why it's needed

ADL automatically reduces the leverage involved in the platform's aggregate position. Although it may appear harmless, in practice it results in the forced closure of profitable positions.

The logic is simple: when someone's position goes deep into the red and gets liquidated, the exchange needs to find a counterparty to close that position. Usually, an insurance fund is used for this. But if losses are too large and the fund isn't enough, the exchange turns to the opposite side of the trade – those sitting in profit.

Gleb Kostarev, former Vice President of Binance for Eastern Europe and CIS (worked at the company from 2018 to 2023), explained the Hyperliquid situation this way:

Yes, of course, Hyperliquid has an ADL mechanism. ADL is the last line of defense for any exchange, even a decentralized one. Hyperliquid has a huge insurance fund of $3.5 billion, but even with that, they must always have additional mechanisms (just in case) that won't allow the exchange to go into the red.

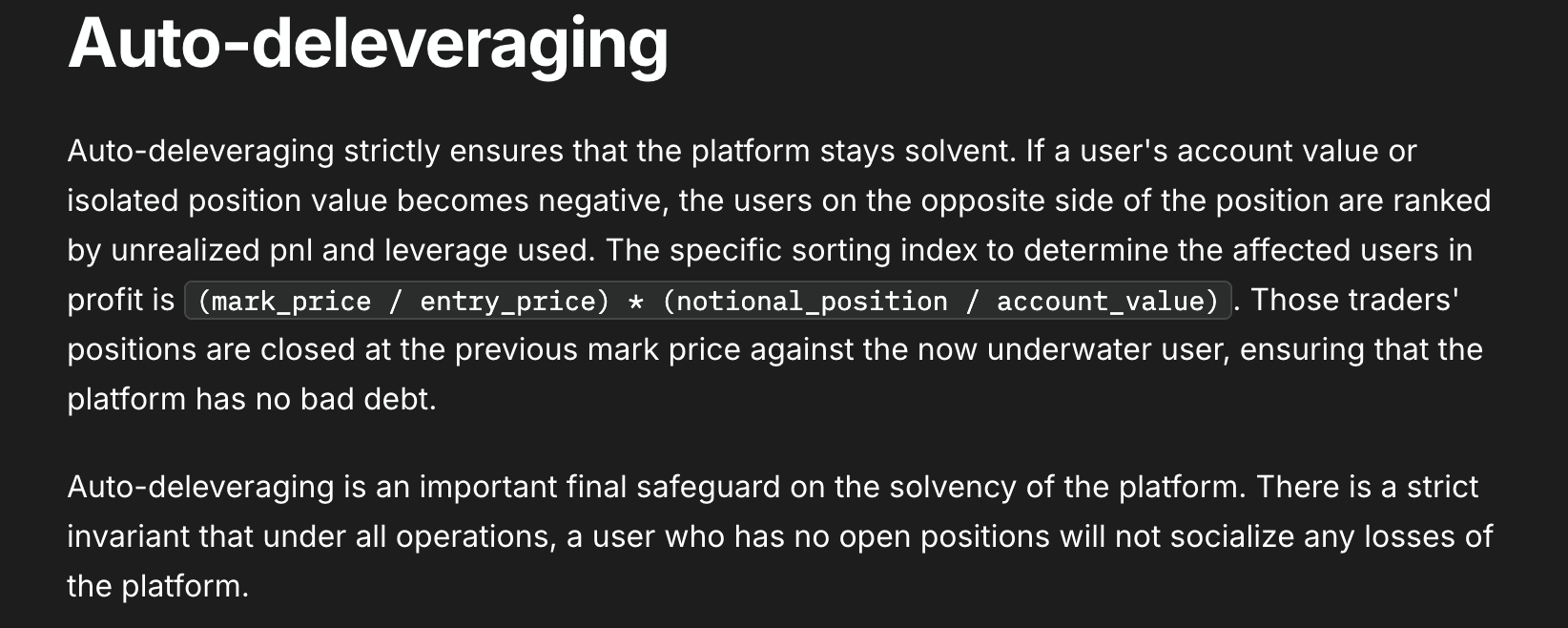

According to Hyperliquid documentation, if a user's account balance or isolated position value becomes negative, the system ranks traders on the opposite side by unrealized profit and leverage used.

The higher this indicator, the sooner a trader’s position may be subject to ADL.

DEX vs CEX: is there a difference

Supporters of decentralized exchanges often talk about transparency. They say that on CEXs the ADL mechanism is a black box, while on DEXs everything is on smart contracts, out in the open. Technically, that's true. All trades on Hyperliquid are recorded on the blockchain, anyone can verify.

But Kostarev notes the practical side:

This is correct; in this respect, CEXs are not significantly different from DEXs. When your profitable position gets liquidated during a crash, what's the difference in the end?

ADL is an exchange survival mechanism, not an ideological choice. Centralized or decentralized – doesn't matter. If the exchange risks going into the red, it will protect itself at users' expense. The only question is how often this happens.

October crash: the Hyperliquid case

Hyperliquid launched in 2023 and until October 2025 operated without a single ADL activation. This was its competitive advantage. An insurance fund of $3.5 billion looked serious. But the October 11 crash was so sharp that the mechanism finally triggered.

Within hours, Bitcoin dropped from $126,000 to around $104,000. On Hyperliquid, over a thousand accounts were completely liquidated. More than 6,300 accounts went into loss totaling over $1.23 billion. This does not include traders whose profitable positions were forcibly closed through ADL.

Many affected were market makers and quant funds holding hedged portfolios. When ADL closed part of their positions, their hedge collapsed, and they were left unprotected against further price movement. Spencer Hallarn, Head of OTC Trading at GSR, called this "a complex problem" for participants with multi-component portfolios.

Why ADL Is Inevitable

The insurance fund isn't infinite. It's replenished through fees and profits from liquidations, but during sharp market movements it may not cope. And then the exchange has three options:

- Use ADL (forcibly close profitable positions)

- Go into loss (and go bankrupt)

- Socialize losses (split them among all users, including those who don't have open positions but have deposits on the platform)

From a risk management perspective, the first option is typically considered the least harmful. At least on DEXs like Hyperliquid there's a strict rule: if you don't have open positions, you don't bear the platform's losses. This is an important detail: losses aren't spread across everyone, but fall only on active traders on the opposite side of the trade.

Can you protect yourself from ADL

Theoretically – no. If you're in profit and holding leverage, you're a potential ADL target. But practically, you can reduce risks:

- Reduce leverage. The lower the leverage, the lower your liquidation priority.

- Lock in profits. The less unrealized profit hangs on the position, the lower your rating in the ADL formula.

- Trade on multiple platforms. Diversification reduces the risk of one exchange closing all your positions at once.

- Monitor liquidity. During high volatility, order book volumes drop, meaning ADL activation probability increases.

It is important to understand that ADL is neither a bug nor a form of manipulation. It's a built-in exchange bankruptcy protection mechanism. And if you trade with leverage, you automatically participate in this system.

Conclusions

The ADL mechanism exists on all major exchanges – both centralized and decentralized. The only difference is transparency: on DEXs you see the algorithm in code, on CEXs—only the consequences.

Hyperliquid operated for two years without ADL activation, which speaks to good risk management. But the October crash showed: there are no perfect systems. When the market moves too fast, even a $3.5 billion insurance fund may not be enough.

Trading with leverage always means risk of forced position closure. And not necessarily a losing one. The exchange will protect its solvency first, and ADL is one of the tools for that.

Even when ADL occurs on a smart contract, the underlying financial mechanics remain the same. A liquidation is a liquidation, regardless of whether it's recorded on blockchain or not.

Recommended